TAK® VERTICAL HORIZON

TAK® VERTICAL HORIZON

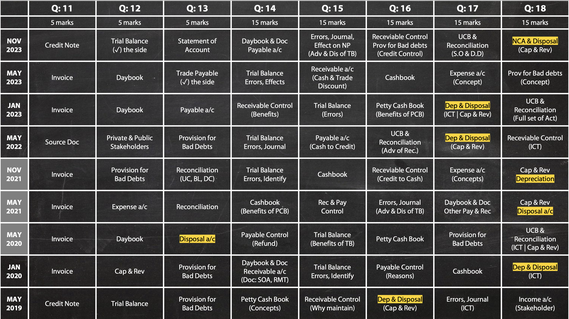

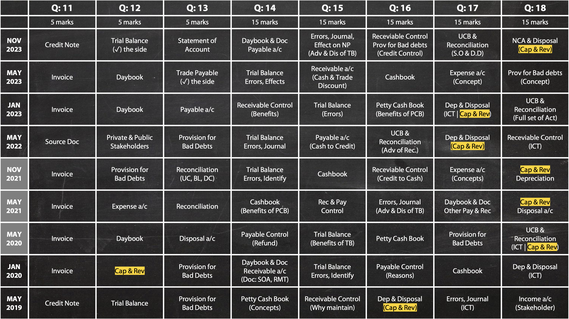

TOPIC 1: BOOKS OF ENTRY & SOURCE DOCUMENTS

EXPECTED QUESTIONS:

- Within each Section A, 5 mark question in every paper, candidates are consistently presented with a task to fill in various documents, typically centered around completing invoices and credit note. This time there is a possible chance of having statement of account.

- Section B consistently features a 15 mark question related to either the petty cashbook or cashbook. Given the presence of a cashbook in the May 2023 paper and none in Nov 2023, it's highly likely that the upcoming paper will include a question on the petty cashbook.

- There is a possibility of a 5 mark question where candidates are required to identify source documents or books of entry.

- There is also a possibility of encountering a question in which candidates may be required to prepare daybooks such as the sales daybook, purchase daybook, return inward daybook, or return outward daybook. In addition to these daybooks, candidates might need to set up the corresponding ledger accounts, including the sales account, purchase account, return inward account, or return outward account. (May 2023 (R) Q:14)

WHAT TO REVISE:

1. Complete the following documents: Invoice, Credit note & Statement of accounts

2. Identify source documents & books of original entry

3. How to prepare three column cashbook

4. How to prepare petty cashbook

5. How to prepare sales, purchase, return inward & outward daybook (May 2023(R), Q;14)

5. How to prepare discount allowed & discount received account from cashbook

6. How to prepare expenses account from petty cashbook

THEORY

- Benefits of preparing petty cashbook.

- Why petty cashbook balance may differ from the amount in petty cash box. (Jan 2023, Q:16c)

- Definitions/ Purpose for different types of source documents (Jan 2020 Q:14)

IMPORTANT TIPS:

1. How to calculate discounts for both before and after payment in cashbook (Nov 2021 Q:15, check transaction on 16 Aug and 30 Aug)

2. How to restore petty cashbook both at the end and beginning of the month.

TOPIC 2: IRRECOVERABLE DEBTS

EXPECTED QUESTIONS

In Section A, there may be a concise 5-mark question in which candidates are required to calculate or prepare a provision account.

WHAT TO STUDY:

1. How to calculate provision for irrecoverable debts

2. How to calculate the rate (%) for provision for irrecoverable debts

3. How to prepare irrecoverable debts account

4. How to prepare provision for irrecoverable debts account

5. How to prepare irrecoverable debts recover account.

6. State the treatment of provision for irrecoverable debts in financial statement.

7. Journal Entry for recording irrecoverable debts, provision for irrecoverable & bad debts recover

THEORY:

1. Explain how prudence concept in applied in calculation of provision for irrecoverable debts

2. Distinguish between irrecoverable debts and provision for irrecoverable debts

3. Credit control policy (i.e. how to reduce irrecoverable debts)

TOPIC 3: DEPRECIATION

EXPECTED QUESTIONS:

Within Section B, there is a strong possibility of encountering a 15-mark question that necessitates the creation of a provision for depreciation and disposal account. Furthermore, this question may include an additional 5-mark component, assessing your evaluation of the application of accrual concepts in depreciation.

WHAT TO STUDY:

1. Calculation of depreciation using both straight line and reducing balance method

2. How to prepare non current assets account

3. How to prepare provision for depreciation account

4. How to prepare disposal account

5. State the treatment of depreciation in financial statements.

6. Journal Entry for recording depreciation and disposal.

THEORY

1. Definition of depreciation

2. Four factors of depreciation

3. Application of accrual concepts in calculation of depreciation

4. Application of consistency concepts in change in depreciation method

5. Evaluate the effect on financial statements of a change in the depreciation method

IMPORTANT TIPS:

- It's essential to thoroughly review the question to determine whether a monthly calculation is necessary for yearly depreciation. So far, all questions have adhered to the policy of "No depreciation in the year of sale and full depreciation in the year of purchase," which didn't require monthly calculations.

- When creating a disposal account, ensure that all transaction dates are specified, and include a closing date to facilitate account reconciliation.

- On the credit side of the disposal account, provide detailed information for the total depreciation of the sold assets as "provision for depreciation." It's important to avoid the common mistake of merely writing "(depreciation)," as this has resulted in candidates losing marks.

TOPIC 4: LEDGER ACCOUNT

EXPECTED QUESTION

There can be a question related to other payable and receivable. There is a possible chance of having a question where candidates will be asked to prepare income or expense account.

WHAT TO STUDY:

1. Income account

2. Expense account

3. Inventory account

4. How to adjust other payable & receivable

5. State then treatment of other payable & receivable in financial statement

THEORY

1. State the treatment of other payable & receivable in preparation of financial account

2. Define other receivable and payable

3. Application of accrual concepts in adjusting other payable & receivable

IMPORTANT TIPS:

Dates, Details & Amount must be mentioned properly when preparing "T" account. Mark will be provided combining all three.

TOPIC 5: CAPITAL & REVENUE EXPENDITURE

EXPECTED QUESTION

Every year, a question worth 5-10 marks is allocated to this particular topic. Usually, students are required to identify between capital and revenue expenditures, while the rest of the questions revolve around theoretical concepts.

WHAT TO STUDY:

1. What is capital expenditure

2. What is revenue expenditure

3. Explain the effect on incorrect treatment of capital & revenue expenditure

4. Application of materiality concepts in treatment of capital & revenue expenditure.

TOPIC 6: CONTROL ACCOUNT

Expected Questions:

In section B, there is a significant likelihood of encountering a question related to this topic, where you might be required to prepare either a control account or an individual account . This question will account for 15 marks. Ensure that you have a strong grasp of both trade payable and trade receivable accounts.

WHAT TO STUDY:

1. Prepare Trade receivable control account

2. Prepare Trade payable control account

3. Prepare individual account for a customer (i.e. trade receivable a/c)

4. Prepare individual account for a supplier (i.e. trade payable a/c)

THEORY

1. Reason of preparing control account

2. Benefits of preparing control account

3. Reason of having abnormal balance or refund

4. Definition/ Reasons/ Benefits for cash discount and trade discounts

5. Evaluate the proposal to sale inventory on cash (Nov 2021, Q:16)

6. Evaluate the proposal to sale inventory on credit (May 2022, Q:15)

IMPORTANT TIPS:

- While preparing ledger account, give all details referring to day book. (such as Cashbook for bank)

- For personal account, all entries are recorded at transaction dates.

- For control all entries are recorded at closing date.

TOPIC 7: TRIAL BALANCE & ERRORS

Expected Questions:

- Each year, particularly in section B, there is consistently a 15 mark question focused on this topic in the examination. Candidates are tasked with preparing a trial balance in response to this question.

- Additionally, there might be another question requiring candidates to identify or rectify errors in financial records using journal entries.

- It is noteworthy that, until now, there has been no request for candidates to prepare a suspense account. However, considering the dynamic nature of exams, candidates should remain vigilant and prepared for potential changes in the examination format.

WHAT TO STUDY:

1. Trial Balance

2. Identify types of errors

3. Prepare Suspense account

4. Effects on profit, working capital or capital after correction

THEORY

1. Reason for preparing trial balance

2. Benefits of trial balance

3. Drawbacks/ Limitation of trial balance

4. Explain different types of error

5. Explain those errors which create difference in trial balance

TOPIC 8: BANK RECONCILIATION

EXPECTED QUESTIONS

The likelihood of this chapter appearing in the exams is relatively low. It may be included in either Section A or Section B. Combining problem-solving and writing theories in your responses could result in a scoring range of 5 to 10 marks.

WHAT TO STUDY:

1. Prepare Updated Cashbook

2. Prepare Bank Reconciliation

THEORY

1. Purpose of preparing updated cashbook and bank reconciliation

2. Advantages & Disadvantaged of preparing bank reconciliation statement

2. Difference between standing order and direct debit

4. Explain dishonoured cheque, bank lodgement and credit transfer

TOPIC 9: ACCOUNTING CONCEPTS

EXPECTED QUESTIONS

1. Importance of using accounting concepts and principle while preparing financial statements

2. Define accrual, prudence, consistency, materiality and business entity concepts

3. Explain the application of prudence concepts in calculation of provision for irrecoverable debts.

4. Explain the application of accrual concepts in recording depreciation

5. Explain how consistency is applied for choosing one method for depreciation

6. Application of materiality concepts in treatment of capital & revenue expenditure

7. Benefits of maintaining a full set of accounting records

TOPIC 10: COMPUTERISED ACCOUNTING (ICT)

EXPECTED QUESTIONS

1. Advantages & Disadvantages of introducing computerised accounting in a business

2. State two ways to protect the security of electronic data

TOPIC 11: TYPES OF BUSINESS & PROFESSIONAL ETHICS

EXPECTED QUESTIONS

1. Distinguish between private sector and public sector

2. State all the stakeholders and their interest

3. Advantages & Disadvantages of operating a business as a sole trader

4. Advantages & Disadvantages of operating a partnership business

5. State all the fundamental principle of professional ethics

In recent times, there have been significant fluctuations in O-level grade boundaries. Starting from May 2020, in response to the pandemic, grade boundaries were notably lowered, providing candidates with a substantial advantage in achieving high scores. This trend persisted until January 2023. However, come May 2023, there was a remarkable upward adjustment in the grade boundaries, making it more challenging to attain honors grades.

As of now, candidates are strongly advised to aim for a minimum of 105 marks to secure a Grade 7. Achieving a Grade 9 necessitates extreme precision and accuracy in your examination paper, with a minimum target of 130 marks. For a comprehensive overview of grade boundaries from previous years, please refer to the chart above.

For further queries and feedback please comment below

my name is name nothing to know my name (Thursday, 06 June 2024 14:56)

?>?>>????

Ashley Wright (Wednesday, 29 May 2024 00:35)

i love niggas

Arian (Monday, 13 May 2024 20:28)

TAK sirr besttt

Yushra zabin (Friday, 10 May 2024 23:29)

This is instructions are really really helpful it’s helping me a lot through my accounting journey.

Fahmida Haider (Thursday, 09 May 2024 08:16)

Truly an amazing website. Really helped me during my mocks. Also love how it's so organised and well maintained. Thank you so much for this.

Mustansir Kutubuddin (Wednesday, 08 May 2024 21:51)

Really helpful guideline as the precise information of past papers is gathered which gives an idea of important topics and therefore helps to prepare for exams

Zawaad Arvin (Wednesday, 08 May 2024 21:48)

The way it is organised is truly very helpful and easy to understand, the hardwork must be appreciated of the teacher! Thanks a lot

Nicholas Tesla (Wednesday, 08 May 2024 21:18)

I appreciate the straightforwardness of the information provided, rather than inundating with unnecessary details. It demonstrates a respect for student's time by precisely indicating what to study, instead of just mentioning the topic's name without delving into its contents. This approach makes it easier for students to quickly identify what they need to focus on.

Rohan (Monday, 06 May 2024 22:50)

Thanks for the guideline. it was really helpful. It make my work very organized.

Eleni (Saturday, 04 May 2024 17:29)

State three reasons why a business may receive a refund from a credit supplier

ATNAGID (Monday, 08 April 2024 17:23)

Sir please do the same for the may 24 candidates like us

not preferred to say (Thursday, 16 November 2023 15:00)

sir, may i know will you post for paper 2, too?